Best LoanDisk Alternatives for Microfinance and Small Lenders (2026)

Nobody goes looking for a LoanDisk alternative on a good day. You go looking when your accountant asks for a clean trial balance the system fights you on, or when you open your third branch and realise you genuinely can't tell which one is making money, or when you find yourself exporting to a spreadsheet, again, to answer a question the software should have answered for you.

If that's where you are, this page is for you. Full disclosure up front: we build a loan management software (LMS) ourselves — Lendbox is our product, and it's profiled below alongside everyone else. So read our section with that in mind. But we've spent years inside the day-to-day operations of small and growing lenders across Africa, Southeast Asia, and South Asia, and most of what follows is just an honest read of where each tool helps and where it gets in your way.

LoanDisk is cloud-based, used in 60-plus countries, and cheap, it starts at $59/month, the trial is 45 days with no card, and there's no setup fee. That's the case for it, and it's a real one at small scale. The case against it is what this whole page is about: it's a thin individual-loan tracker, and the gaps show up fast the moment you grow past that.

Start with what it isn't built for. The plan ceilings tighten as you scale: $59 buys one user and 2,000 loans, multi-user doesn't start until $129, and you don't get unlimited until $346/month — so the "cheap" headline erodes the bigger you get.

Quick pick

- Best for Kenyan MFIs that collect in the field and need mobile money: Musoni — M-PESA and Airtel integration plus an offline field-officer app.

- Best for lenders who need real accounting, group aging, and branch-level control without an enterprise budget or a developer: Lendbox (ours).

- Best for South Asian NBFCs and co-operatives: Cloudbankin — built around Indian lending and RBI-shaped reporting.

- Best budget option: Lendbox, from $19/month.

- Only if you're building a digital bank with an engineering team: Mambu — powerful, API-first, and almost certainly overkill for you.

The tools, one at a time

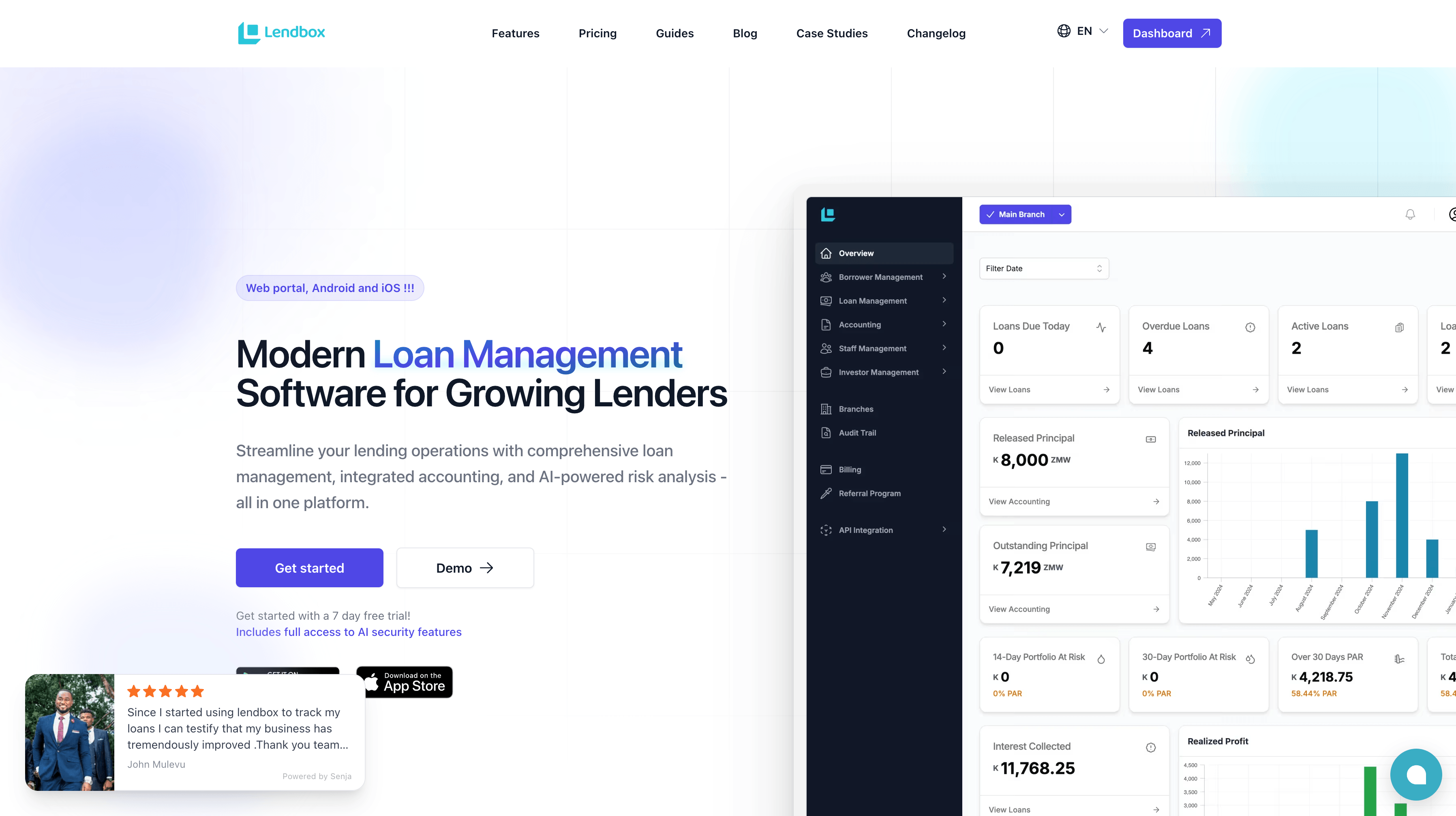

1. Lendbox

Full disclosure: Lendbox is our product. We'll keep this as straight as the rest.

Lendbox is built specifically for small and growing lenders in emerging markets, the ones who've outgrown Excel but would be crushed by an enterprise core-banking project. It also starts at $19/month, which undercuts most of this list and roughly a third of LoanDisk's entry tier, so "graduating to real software" doesn't have to mean a bigger bill.

What you get for that is the stuff that usually breaks first as you scale. Double-entry accounting is built in, not bolted on, with a shared chart of accounts across branches, so consolidated books and per-branch P&L come out of the same ledger your loans post to — not a separate accounting app you reconcile by hand. Repayment allocation follows a real waterfall — Penalties → Fees → Interest → Principal → Overpayment — so what a borrower owes and what your books say never drift apart. Group lending comes with 30/60/90 aging buckets, and multi-branch is the genuine thing: branch-level attribution plus approval workflows (Branch Loan Officer → Branch Manager → Manager → Super Admin), so control doesn't evaporate when you add locations. There's also AI credit scoring to help size up a borrower's risk before you disburse, rather than going on gut and a paper file. Rounding it out: a borrower portal, SMS/Email/WhatsApp notifications, a collateral register, and document e-signing.

Where we're honest about the gaps: we don't currently offer a native mobile-money integration that auto-reconciles an M-PESA or mobile-wallet feed — if that's the single most important thing in your operation, Musoni is stronger there today. And we're focused on the lending-plus-accounting core, so a fully deposit-taking institution running large savings and share-capital books should check that scope against ours before deciding.

Suits: small-to-mid lenders who need accounting, group aging, and branch control done properly. on a budget, and without a developer.

2. Musoni System

Musoni is what LoanDisk isn't: a proper microfinance core system, built on the open-source MifosX platform, with deep roots in East and Southern Africa (Kenya, Uganda, Tanzania, Zimbabwe, Ghana) and use across roughly 19 countries. It does clients, groups, loans, savings, shares, and integrated accounting, and — the real differentiator — it ships a Digital Field Application that works offline, so loan officers can capture data and collections in areas with no signal and sync later. Its mobile-money integrations (M-PESA, Airtel, Payway) are first-class, not bolted on. If your model is group lending with field collection over mobile money, Musoni is built for exactly your day.

The trade-offs are cost and weight. The "Musoni Starter" tier runs around €999/month, and the full system is priced by institution size — a real step up from LoanDisk's $59. The client-facing app is deliberately minimal (Musoni positions it as a starting point you extend yourself), and multi-currency on the financial side has been a noted limitation by long-time users. It's also more system than a two-person lender needs.

Suits: growing MFIs and SACCOs doing group lending and field collection, ready to pay for digitisation. Overkill for: a solo money lender with a few hundred individual loans.

3. Cloudbankin

Cloudbankin (from Habile Technologies / LightFi, Chennai) is a SaaS banking engine covering loans, savings, deposits, shares, collections, and accounting, and it's tuned tightly to the Indian market — NBFCs, MFIs, and co-operative societies. The reason to choose it is the same reason it's narrower for everyone else: it speaks RBI. GST handling, NPA memo accounting, branch and product-wise reporting, trial balances and balance sheets in the formats your auditor and regulator expect — that's all native. It supports multi-currency and configurable charges (disbursement, overdue, EMI bounce, foreclosure), and it's genuinely strong for the JLG-heavy group lending common in Indian microfinance.

The honest caveats: it's a comparatively newer platform, and users flag the reporting and reconciliation modules as still maturing, with some setup effort and occasional data latency. Its local rails are Indian — UPI, eKYC, account-aggregator flows and pricing is quote-based, not public.

Suits: Indian and South Asian NBFCs, MFIs, and co-operatives that need regulator-shaped reporting out of the box. Skip if: you're outside the South Asian regulatory world.

4.Mambu

Mambu is excellent, and including it is mostly to save you a sales call. It's a composable, API-first, cloud-native core banking platform used by neobanks, fintechs, and digital lenders to assemble exactly the product they want. It has no published pricing because it's an enterprise sale, and it expects you to bring a development team — there's no out-of-the-box end-user mobile app; you build your own against the API. For a lender graduating off spreadsheets, that's the opposite of what you need: you'd spend a year and a serious budget building what a packaged tool gives you on day one.

Suits: funded fintechs and digital-first lenders with engineers, building a custom stack at scale. For everyone else this page is written for: this is the tool to revisit in five years, not now.

Two names you'll see on generic "best LMS" lists that we left off on purpose: LoanPro and Bryt. Both are solid, but they're built for US lending — ACH rails, US credit-bureau reporting, US compliance — and that orientation makes them a poor fit outside that market. Don't let a directory talk you into them for an African or Asian operation.

How to choose

Forget the feature checklist for a second and find yourself in one of these.

You're a solo money lender. Don't over-buy. LoanDisk at $59 is hard to beat for individual lending at small scale, and "stay where you are" is a legitimate outcome of reading this page. Only graduate up when group lending, real accounting, or multiple branches become things you actually do, not things you might do someday.

You're a small MFI doing group lending. Group workflows and aging are non-negotiable, which rules out individual-first LoanDisk. If you also collect in the field and run on mobile money, Musoni's offline field app earns its premium. If your collection is less field-heavy and accounting discipline matters more, Lendbox covers the group-aging-plus-books combination at a lower entry point.

You're a multi-branch lender feeling the ceiling. Everyone here claims multi-branch; the difference is attribution. Ask the demo to show you a per-branch P&L from the same ledger as the loans, and an approval chain that actually stops a branch officer from disbursing above their limit. LoanDisk gives you unlimited branches cheaply but thinner branch-level financial separation; Lendbox and Musoni give you real attribution and controls.

You're a SACCO or credit union. The deciding question is whether you're deposit-taking. If members' savings and share capital are a big part of what you manage, you need full savings/shares/deposit handling — Musoni or Cloudbankin are built for that. If you're credit-led (member loans with light contributions) and your real pain is accounting, branch consolidation, and group aging, a lending-plus-accounting tool like Lendbox fits without the weight of a core-banking system. Map your savings book honestly before you pick.

Bottom Line

Give LoanDisk its due. It's cheap, it's simple, it's been proven across 60-plus countries, and for a single-branch shop lending to individuals it does the job without fuss or a big bill. If that's you, staying put is perfectly alright — and we'd rather tell you that than sell you something you don't need.

But you don't usually end up on an alternatives page unless you've hit a wall, and LoanDisk's walls are predictable: group lending it can't really model, accounting that's bolted on rather than built in, and "many branches" that doesn't translate into clean per-branch books. Those are exactly the things that decide whether you can scale without your back office unravelling. Lendbox was built for that moment — double-entry accounting at the core, a real repayment waterfall, group aging, and genuine branch-level control — and it starts at $19/month, so moving up doesn't mean paying more.

If your wall is accounting, group aging, or branch control, the next step is small and reversible. Try free for 7 days. Import your Excel in one afternoon. No card needed. lendbox.io